Indian entrepreneurship, innovation, and business firms have gone through a plethora of changes, particularly in the last three decades. The most significant change is the result of national government policies that had the effect of moving away from postcolonial Nehruvian socialism and creating a climate for more economic freedom for entrepreneurs and private businesses. The 1990s was the watershed decade for these revolutionary changes. Indian business suddenly took off with a new outburst of energy and enthusiasm in the 1990s that was unprecedented in the post-Independence era.

In the 1990s, India made a transition from an inward-looking democratic socialist economy that often discouraged international trade/investment and allowed private business but overregulated it to a set of market reforms that brought in foreign investments, connected India to the global market, and created opportunities for Indian companies to venture abroad. A large range of actors, both in formal (regulated by government policies) and informal sectors (unstructured markets, not monitored by government regulations) juggled to secure their own niches in new waves of policy changes, globalization trends, and competition from foreign investments.

India’s upward development curve jumpstarted the service sector, encouraged entrepreneurship and innovation, created global business leaders, and institutionalized the jugaad phenomenon, a unique Indian characteristic that motivated Indians to struggle and prosper.1 Jugaad, a Hindi word, is usually identified with disruptive and innovative strategies at different levels in Indian business that is very organic in nature. It is a way of dealing with everyday problems for Indians and attempting to find solutions independently of any organizational support or intervention. In an overpopulated, competitive market, it has enabled Indians not only to survive, but also innovate. It is sometimes referred to as “frugal engineering.” New government policies that made use of cultural propensities and economic incentives have dramatically altered India’s business climate since the democratic socialist model was altered. As a consequence, in the World Bank report from 2018, The Ease of Doing Business, India jumped ahead by 23 spots to the 77th overall position from 100th place in 2017.2

The remainder of this essay is a brief historical introduction to the Indian economy during British colonialism, India’s economic policies over three decades after Independence, and the events that changed the lives of entrepreneurs and many ordinary people after the 1990s. Challenges and opportunities for businesses and India’s economy are briefly discussed at the end of the essay.

Legacies of the Past

Caste/region/language—or religion-based business communities—prevailed for centuries in India before the advent of colonial rule. The colonists catalyzed disruptions in traditional trading patterns, as well as shifted economic power to colonial masters. British rule led to the considerable decline of old family firms and, in turn, introduced new methods of banking, managing agencies, and chambers of commerce that fluidly connected the Indian subcontinent to the global economic order. The new players in business were both foreign and local. Traditional business communities like Sindhis and Chettiars3 reorganized their operational structures and mechanisms, and others worked with the British as mediators and administrators (dobash: interpreters, banians: traders and middlemen), and also invested in trade and commerce. Expansion of internal markets and profitable Chinese trade, particularly in cotton and later opium, led to the flourishing of Indian business and the emergence of the Indian private business class by the beginning of the twentieth century.

Joint family ownership and hereditary business continued, and many prominent names emerged. The Birlas, for example, who belonged to the traditional business caste from Rajasthan, started as opium and jute traders in Calcutta (Kolkata) and later invested in the jute, cotton, sugar, chemical, paper, and insurance sectors. Some other names also emerged from the nontraditional business castes, such as the Kirloskars, who had Maharashtrian brahmin lineage. They were one of the earliest to venture into engineering industries in India, producing pumps, compressors, electric motors, transformers, etc. The big business groups of Bombay (now Mumbai) formed powerful pressure groups in the 1920s and 1930s, with many of them lobbying in support of the Indian National Congress and the national movement against the British rule over India.

Many indigenous business houses acquired flourishing, mostly British expatriate companies as the owners made hasty retreat with the political and economic changes.

The post-Independence era (post-1947) presented a new political climate for Indian business. There was growing antipathy toward capitalistic freedom (often synonymized with colonialism) and private enterprise that was fueled by the “socialistic” mindset of Nehru, the first Indian prime minister. He favored government control of the economy, structured economic planning, and the dominance of the public sector, but allowed a mixed economic model without eradicating the private sector. With the regulatory acts of 1951 and 1956, the government could determine location of industries, quantities, production, price, and distribution of products. Thus began the era of the “license raj” for the next fifty years, where control by the government set the dominant narrative of Indian business. Nehru was inspired by the Soviet model and economic practices of Communist China. Yet Indian business groups were not totally demotivated, as they were left undisturbed in areas of consumer products in a huge domestic market. The politically influential owners of private big businesses worked and invested in developing mutually supportive relationships between government and bureaucracy that sometimes included “insider information” that could cause owners to invest or refrain from particular business endeavors.

Regulations became more severe during Indira Gandhi’s (Nehru’s daughter) governments (1966–1977, 1980–1984). She nationalized major banks (1969), and introduced restrictive trade acts (1969) and foreign exchange regulations (1973). In her governments, the number of foreign firms rapidly declined, public-sector undertakings expanded, and fewer private businesses were created than in earlier post-Independence governments.

With some exceptions, Indian big business did not suffer too badly during the “license raj” period. There were advantages of the large domestic market, freedom from foreign domination and market controls, the acquisition of retreating foreign companies, and opportunities for floating new ventures. Many indigenous business houses acquired flourishing, mostly British expatriate companies as the owners made hasty retreat with the political and economic changes. Also emerging were new names who started from scratch and flourished, like that of Dhirubhai Ambani, founder of Reliance Industries, who started in the textile sector but later ventured into petrochemicals, communications, and many diverse sectors.4 However, consumers suffered badly because of few product choices in the market, as did the development of the spirit of enterprise and innovation, along with the quality of products offered with no incentive to invest in research and development. There were very few opportunities and little motivation for new players and new kinds of businesses, and the choicest occupations for the middle class remained those in “service,” particularly “safe and secure” government service.

Economic Reforms and the Re-emergence of Entrepreneurship

Rajiv Gandhi, who assumed the office of prime minister in 1984, nourished visions of creating technological changes in India. There was already growing disillusionment with the public sector, lesser apathy toward the private sector, and a greater realization of the necessity of economic reforms. However, not much changed in the 1980s except in the telecommunications sector, which was transformed by the Centre for Development of Telematics (C-DOT) under the visionary technocrat Sam Pitroda and his team of software professionals. The major turnaround took place with the assumption of office of PM Narasimha Rao in 1991 after the untimely death of Rajiv Gandhi.

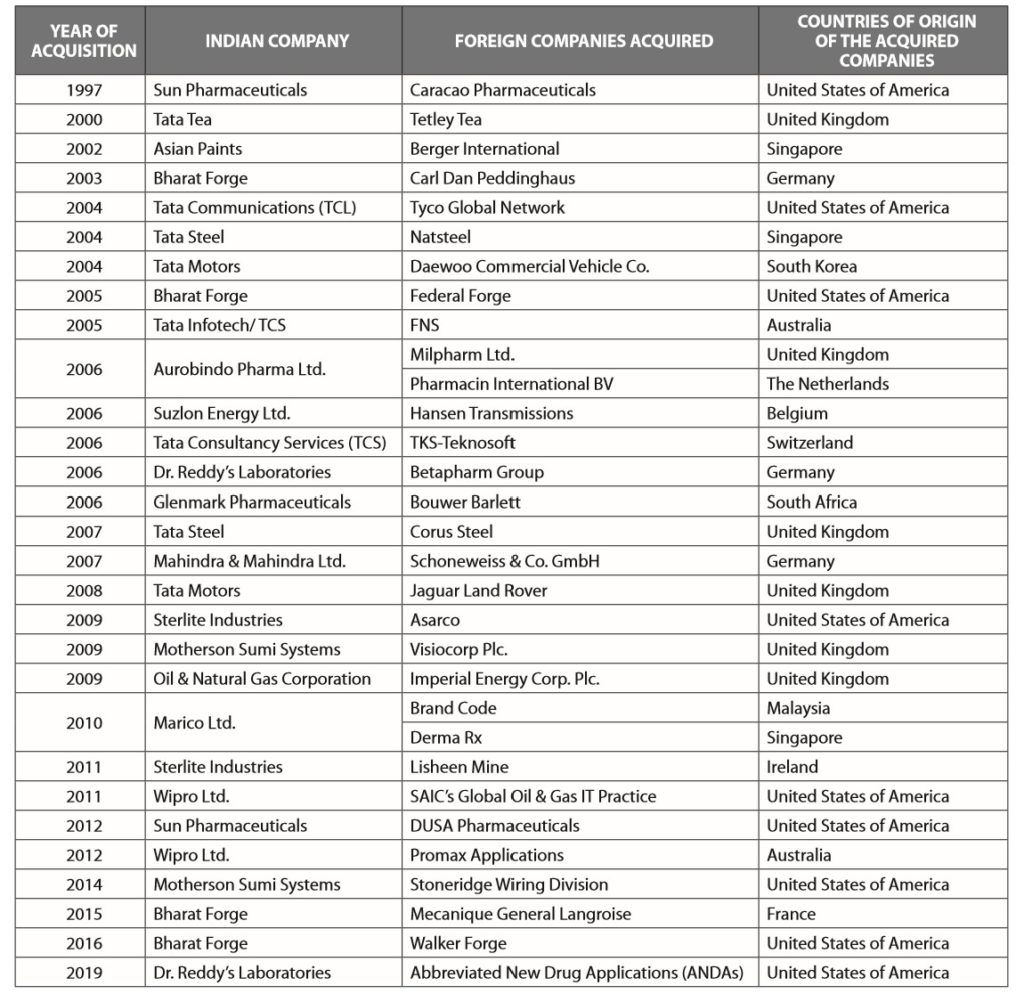

Table 1:

Some Popular Mergers and Acquisitions by Indian Companies

Rao had the advantage of moving beyond the burden of the Gandhis’ socialistic legacy. Much as there was an ideological acceptability of the necessity of reforms, it was actually triggered by the country’s acute current account deficit in 1990. At one point, India’s foreign exchange reserves fell to a cash equivalent of two weeks’ imports. Rao appointed Dr. Manmohan Singh, a Cambridge-trained economist, who succeeded Rao (2004–2014) as his finance minister, to the surprise of many. The Rao–Singh team created history and reversed the country’s fortunes. The new industrial deregulation, delicensing, and export-oriented policies did away with the “license raj” and opened new horizons for private enterprises. Tariffs on intermediate goods were reduced, encouraging exports, and banking sector and stock market reforms were initiated. Economic growth rates catapulted to 9 percent between 2003 and 2007, later moderated to 5.6 percent (2012) and 8 percent (2015–2016).

With the allowance of private investments into the traditional public sector, industries like telecommunications, electronic media, and civil aviation benefited greatly.

The reforms changed the Indian business environment completely. Many first-generation entrepreneurs took progressive steps away from traditional caste-based lineages. They were largely driven by opportunities of entrepreneurship, the increased benefits accrued from their individual educations, and the potential of technology dramatically improving business operations. Economic liberalization facilitated the process by linking this progression with globalization. Indian businessmen had to rethink and reorganize their business models to be competitive with the rest of the world and to confront the foreign companies making inroads into the Indian market. Family-run firms restructured and consolidated their businesses, closed down unprofitable units, cleaned their balance sheets, and/or diversified into new areas. Such was the case with B. Ramalinga Raju, who moved away from his family business of construction and cotton spinning to set up Satyam Computers in 1992. The importance of enhancing professionalism was emphasized, especially with a new and educated (many abroad) generation of family businesses ownership. These first-generation entrepreneurs were mostly driven to technology-based sectors like IT and telecom.

The new sectors that flourished were pharmaceuticals, automobiles, and communications technology-based industries (information technology, telecommunications, etc.). The groundwork had been laid in the 1980s, but 1990s liberalization mobilized their takeoff on a different scale and magnitude. Among pharmaceutical companies, Lupin Laboratories, Sun Phamaceutical Industries, and Dr. Reddy’s Laboratories were incorporated in 1980, 1983, and 1984, respectively. Similarly, Wipro by Azim Premji, Shiv Nadar’s Hindustan Computers, Tata Consultancy Services (TCS–Tata Group), and Infosys by Narayan Murthy all had their origins in the 1980s, and a majority of these leaders were also first-generation entrepreneurs.

Market liberalization led to an influx of foreign investors who were quick to realize the market potential and cheap labor advantages of India. In the field of automobiles, one of the earliest entrants was the South Korean firm Daewoo Motors in a fifty-fifty joint venture (JV) with DCM Toyota. Others such as Hyundai, Mitsubishi, Honda, General Motors, Ford, and Mercedes-Benz soon followed, injecting technical and manufacturing skills into the sector. It forced the indigenous carmakers to launch new and modernized models, like Tata Motors did with Indica and Tata Safari (SUV model). Indian consumers began to be exposed to different choices, and market competition led to greater affordability. Passenger cars were no longer considered luxury items by the expanding and consumption-hungry rising middle class, thus bringing about profound social changes in India.

With the allowance of private investments into the traditional public sector, industries like telecommunications, electronic media, and civil aviation benefited greatly. The revolution in the telecom sector was reflected in the spectacular growth of cellular phone services. Big domestic players got involved—Aditya Birla Group (Idea), Tatas (Tata Indicom), and Ambanis (Reliance Communications)—forming JVs with the likes of Ericson, Motorola, Nokia, and Hutchinson. One of the most popular market brands was that of Sunil Mittal’s Bharti Telecom (later Bharti Airtel). They expanded their network and JVs much beyond India. The changes in the telecom sector resulted in the transformation of Indians across regions, classes, and language barriers, introducing a new world of connectivity and knowledge generation. India is the second-largest communications market in the world, with a subscriber base of around 1.2 billion as of December 2018.5

The health care sector also went through remarkable changes, particularly in the post-2000 period. With the induction of technology and research and development into the sector, it became more lucrative for large-scale private-sector participants to invest into chains of big hospitals with state-of-the-art facilities and necessary human resources. The private sector now accounts for about 74 percent of India’s total health care expenditure and is expected to reach US $280 billion by 2020.6 Apollo, Narayan Hrudayalaya, and Fortis are some of the big names. Telemedicine is also an emerging trend, and many business groups are making investments in it. Apart from catering to the rising income groups and general health awareness in Indians, they also catalyzed the rising trend of “medical tourism” for incoming patients from abroad, who are attracted by the quality of healthcare at competitive costs.

The start-up journey in India had been inspired by Indian technology firms in Silicon Valley, along with the growth of the internet, the dotcom boom, and the availability of funds through venture capitalists.

India’s New Image in the New Millennium

While the 1990s provided major groundwork for entrepreneurial development, the twenty-first century witnessed Indian companies scaling new heights in diverse trajectories. One significant characteristic of the new decade was the visibility and progression of Indian multinational enterprises (MNEs) and Indian business leaders on a global stage. Between 2000 and 2009, 437 Indian MNEs spent more than US $70 billion on 976 acquisitions.7 Indian firms were aggressively accessing overseas markets, natural resources, technologies, and skills. Competition from foreign direct investment into the Indian market also provided a push to Indian firms to venture abroad, mobilizing integration of the Indian market with the global economy. Most of the outgoing Indian firms used mergers and acquisitions (M&A) and/ or joint ventures rather than investing in green field ventures (building from the ground up) in order to get quicker global recognition. While the majority of these investments entered developed markets, such as the UK, Germany, Switzerland, and USA, to access technology and skills (around 83 percent), Indian firms also targeted emerging markets in Africa, Latin America, CIS countries, and other developing countries (approximately 17 percent).These ventures gave rise to global business leaders with commendable entrepreneurial capabilities. Kumar Mangalam Birla, Narayana Murthy, and Mukesh Ambani were no longer familiar merely to Indians.8

The new-age Indian entrepreneurs were also facilitated by the process of digitization, which has led to platforms for the creation of companies such as Paytm, OlaCab, Flipkart, and Zomato. OlaCab, India’s most popular online cab aggregator at present, does not own their own cabs or employ drivers, but makes business by connecting users to drivers with a technological platform through a cellphone application. Digitization is closely related to the rising “start-up culture” in India. It is usually a technology-driven business idea with a scalable business model that enables the start-up idea to transition into a company with professional management, investors, incubators, and accelerators. It is driven by the innovative energy of skilled technologists or professionals working toward the commercialization of new products, processes, or services. The Indian start-up ecosystem is one of the largest in the world and grew from 7,000 in 2008 to 50,000 in 2018.9 The founders are usually skilled enterprising students, engineers, and/or management graduates between twenty and forty years old.

The start-up journey in India had been inspired by Indian technology firms in Silicon Valley, along with the growth of the internet, the dotcom boom, and the availability of funds through venture capitalists. Without physically investing in a space (as in a manufacturing unit) to set up an enterprise or using the social capital of traditional business networks, these businessmen have created their enterprises by linking sources to the needs of consumers. These companies have revolutionized the concept of traditional Indian enterprise and business acumen, similar to that of America but with unique Indian characteristics.

One of the important features of the contemporary Indian economy is the public–private partnership (PPP). The industrialists, who had been shunned in the post-1947 era, were now encouraged to work along with the government in the post-Reform period. In 2013, PM Manmohan Singh talked about his belief that government and business should be partners in writing the history of development.10 This reiterated the government’s commitment to partnering with the private sector for India’s economic growth. Post-2014, there have been steps taken by the Modi government to promote digitalization,11 start-ups, and the manufacturing sector in several initiatives with the private sector. For example, government collaboration with Tata Consultancy Services to create a digital platform for Indian passport services has benefited over 150 million Indians. Similarly, the Adani Group was chosen to operate several Indian airports.12 The PPP plays an important part in several infrastructure projects and the health care sector, too.13

Reflections

The transition of Indian business brought about radical changes to how Indian entrepreneurs had been conventionally perceived both at home and abroad. The traditional caste hierarchies and business lineages that prevailed in the postcolonial period, added with government apathy, had marginalized their economic progression. Globally, India was perceived to be a developing economy warped with problems and stunted economic growth. The reforms, globalization, digitization, and other changes ushered in a positive outlook that coincided with the “Asia rising” phenomenon and expedited the fruition of innovative entrepreneurial capabilities. In the words of Fareed Zakaria, Indian–American journalist, political scientist, and author, “The Indian private sector has represented the true India—pragmatic, forward-looking, diverse, open to the world.”14 India was finally able to shake off the legacies of colonial orientation and a backward economy.

The Indian growth trajectory, often compared with China’s, was distinct from the Chinese growth model that had been more state-driven development with a large emphasis on the manufacturing sector. Interestingly, the Indian success story was driven by the service sector that was much more organic in nature, though facilitated by government policies. Thus, while some characteristics of entrepreneurship have been prominent, the growth model cannot be neatly structured because of the heterogeneity of the Indian economy. The informal sector plays a big role in the success story; it accounts for more than 90 percent of enterprises, more than 80 percent in employment generation, and around 50 percent of the GDP. It functions with interesting coexistence of traditional methods and business operations, along with disruptive technologies, e.g., giving the option of e-wallets to consumers but not making it mandatory. Jugaad, discussed earlier, may have motivated innovation strategies from primary levels of the economy in an attempt to find solutions to everyday problems, thus leading India to excel in start-up ideas.

Still, in spite of a number of world-class companies and a surging tradition of innovation, India only ranked 68th in the Global Entrepreneurship Index ranking in 2018 (score: 28.4). The main reasons are persisting high costs of setting up businesses, multiple regulatory authorities, rigid labor markets, and a dearth of skilled labor. The contrasts of Indian businesses at different levels—on the one hand, interrelation and inspiration of Silicon Valley techies or global footprints of Indian enterprises and business leaders; on the other, haphazard growth of the retail sector or inevitable but unpredictable thriving of local markets and bazaars—create complexities and challenges, but also offer opportunities in the Indian market in many different ways.

NOTES

1. Jugaad is studied by scholars across the globe. Thomas Birtchnell, “Jugaad as Systemic Risk and Disruptive Innovation in India,” Contemporary South Asia 19, no. 4 (2011): 357–372; Benoit Godin and Dominique Vinck, eds., Innovation: Alternative Approaches to the Pro-Innovation Bias (Cheltenham, UK: Northampton, MA: Edward Edgar Publishing, 2017); Jaideep Prabhu and Sanjay Jain, “Innovation and Entrepreneurship in India: Understanding Jugaad,” Asia Pacific Journal of Management 32, no. 4 (2015): 843–868.

2. World Bank, “Doing Business Report: With Strong Reform Agenda, India Is a Top Improver for 2nd Consecutive Year,” October 31, 2018, https://tinyurl.com/y545ooz9.

3. The Sindhi business community hailed from the northwestern region of the subcontinent and spread globally during the colonial period, mostly dealing with items of trade like silk, curios, and handicrafts from India and China that were valuable to the colonial rulers. For further details, refer to Claude Markovits, The Global World of Indian Merchants, 1750–1947: Traders of Sindh from Bukhara to Panama (Cambridge: Cambridge University Press, 2000). The Chettiars came from the Madras Presidency, who developed into a strong community of moneylenders and spread their activities along with British colonial footprints in parts of Asia like Burma (now Myanmar), Ceylon (now Sri Lanka), and the Malayan Peninsula (now such as Malysia and Singapore). For further details, refer to David West Rudner, Caste and Capitalism in Colonial India: The Nattukkottai Chettiars. (Berkeley: University of California Press, 1994).

4. Dhirubhai Ambani had no background of family business. In the early 1970s, he took advantage of the government scheme to boost foreign exchange reserves. He imported polyester filament in lieu of the export of art silk that he produced. Besides producing textiles, he managed to import polyester yarns, which he also sold to other producers at a high premium. Later, he used convertible debentures to raise capital for further expansion that became immensely successful and popular with ordinary people. Ambanis eventually ventured into petrochemicals and soon became a name to reckon with, after only the Tatas and Birlas. Dwijendra Tripathi and Jyoti Jumani, The Concise Oxford History of Indian Business (New Delhi: Oxford University Press, 2007), 190–191.

5. This is based on information in Indian Brand Equity Foundation (IBEF), a trust established by the Department of Commerce, Government of India, accessed July 4, 2019, https://tinyurl.com/y3luas6n.

6. “Indian Healthcare Industry Analysis,” March 2019, https://tinyurl.com/y4dzpphj.

7. Karl P. Savant, et al., eds., The Rise of the Indian Multinationals: Perspectives on Indian Outward Foreign Direct Investments (Basingstoke: Palgrave Macmillan, 2010), 12.

8. Kumar Mangalam Birla, the fourth generation of the Birla family, took over as chairman of the Aditya Birla Group (spread across different countries) in 1995 at the age of twenty-eight. By 2015, his group’s turnover amounted to US $42 billion. N. R. Narayana Murthy, also known as the “Father of the Indian IT Sector,” is the cofounder of Infosys and an IT engineer himself. He has been listed among the twelve greatest entrepreneurs of our time by Fortune magazine.

Mukesh Ambani, the elder son of Dhirubhai Ambani, is the chairman of Reliance Industries Limited, a Fortune Global 500 company. He is the richest Asian and is among the thirteen richest people in the world in 2019, according to Forbes magazine.

9. Yanogaya Sharma, “Number of Startups in India Grew 7X to 50X in a Decade: KPMG Report,” ENTRACKR, February 7, 2019, https://tinyurl.com/y6f4n45x.

10. See full text of Manmohan Singh’s address at the CII National Conference, April 3, 2013, https://tinyurl.com/yxvrsxkf.

11. The Startup India Scheme was initiated by the government in 2016 with the ambitious campaign, “Startup India, Stand Up India.” More than 15,000 startups have been recognized, generating approximately 15,000 jobs. Similarly, the “Skill India” campaign, or Pradhan Mantri Kaushal Vikas Yojana (PMKVY), was started in 2015 and aims to train over forty million people in different skills by 2022. The government has also launched apps like BHIM and Aadhaar Pay to digitally empower the Indian population.

12. In July 2019, the Adani Group won the bid to operate in three major airports, Ahmedabad, Lucknow, and Mangaluru, for a period of fifty years. It had earlier won bids to operate Jaipur, Guwahati, and Thiruvananthapuram airports as well. “Cabinet Approves Leasing Out Three Major Airports of Airport Authority of India,” The Hindu, July 3, 2019, https://tinyurl.com/y3fma3qa.

13. Pankaj Sinha, “How India Is Using Public-Private Partnerships to Expand Healthcare,” World Economic Forum, January 7, 2016, https://tinyurl.com/y3nbkt8r. A separate website has been instituted by the Department of Economic Affairs for disseminating information on different projects: https://tinyurl.com/y5zbydfq.

14. Fareed Zakaria, “The Private Sector Is India’s True Face—Open, Pragmatic,” interview by Saumya Roy, Outlook India, October, 11 2005.